01 · The map

Where they are. What's next.

No "where do I start." No parallel spreadsheets. The current piece of work is visible, and so is the one after it. You would be surprised how often that alone unblocks a founder.

VentureQu is the quantum venture-building stack. Built for the funds, studios, and programs writing the first check into quantum — and handed to every company on the cap table.

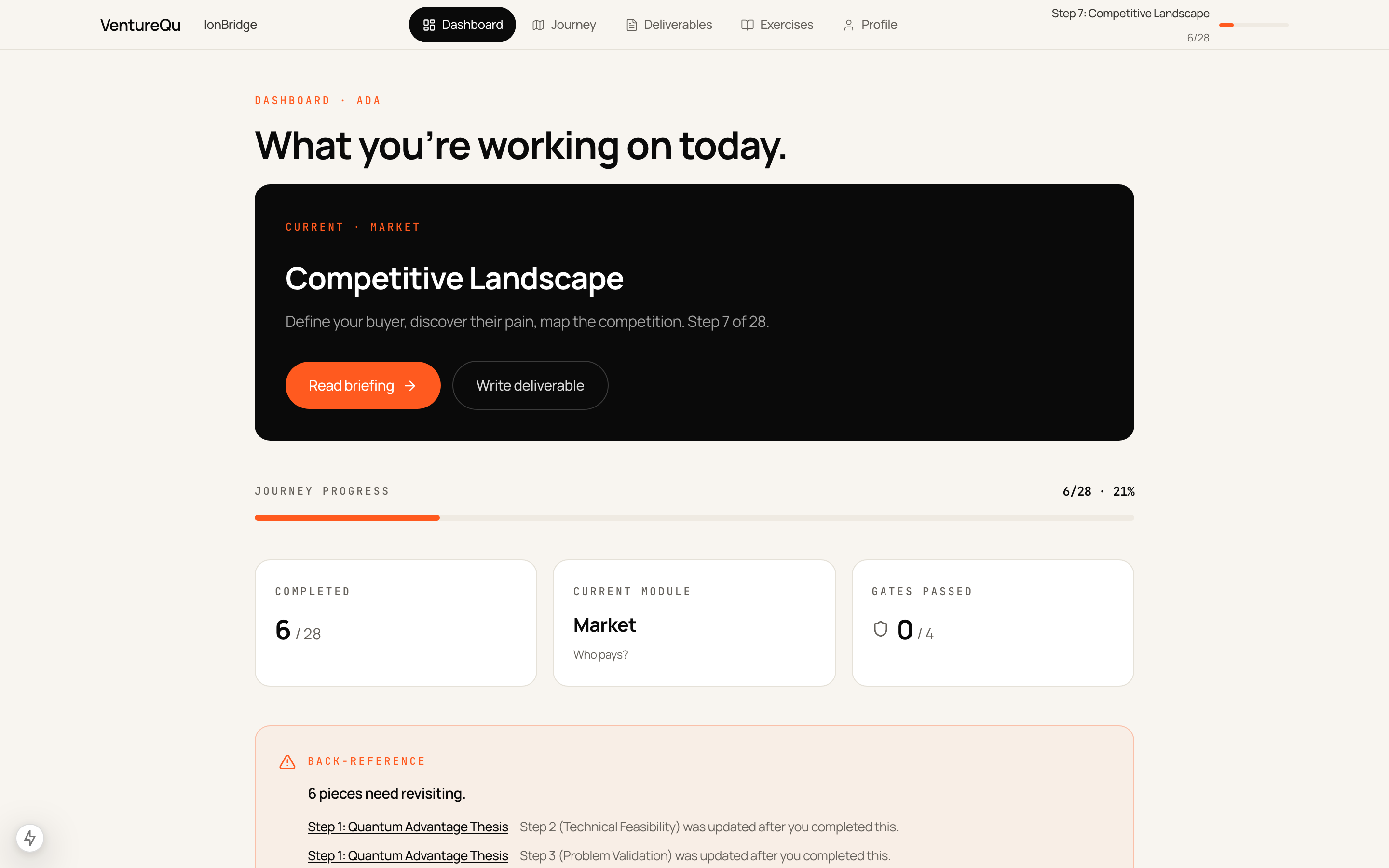

A founder opens the app and knows exactly what to work on today. What "good" looks like. Which rooms their answer will not survive. The decision is in front of them, not buried in a playbook. Most quantum founders are not avoiding the business side. They are drowning in it.

No "where do I start." No parallel spreadsheets. The current piece of work is visible, and so is the one after it. You would be surprised how often that alone unblocks a founder.

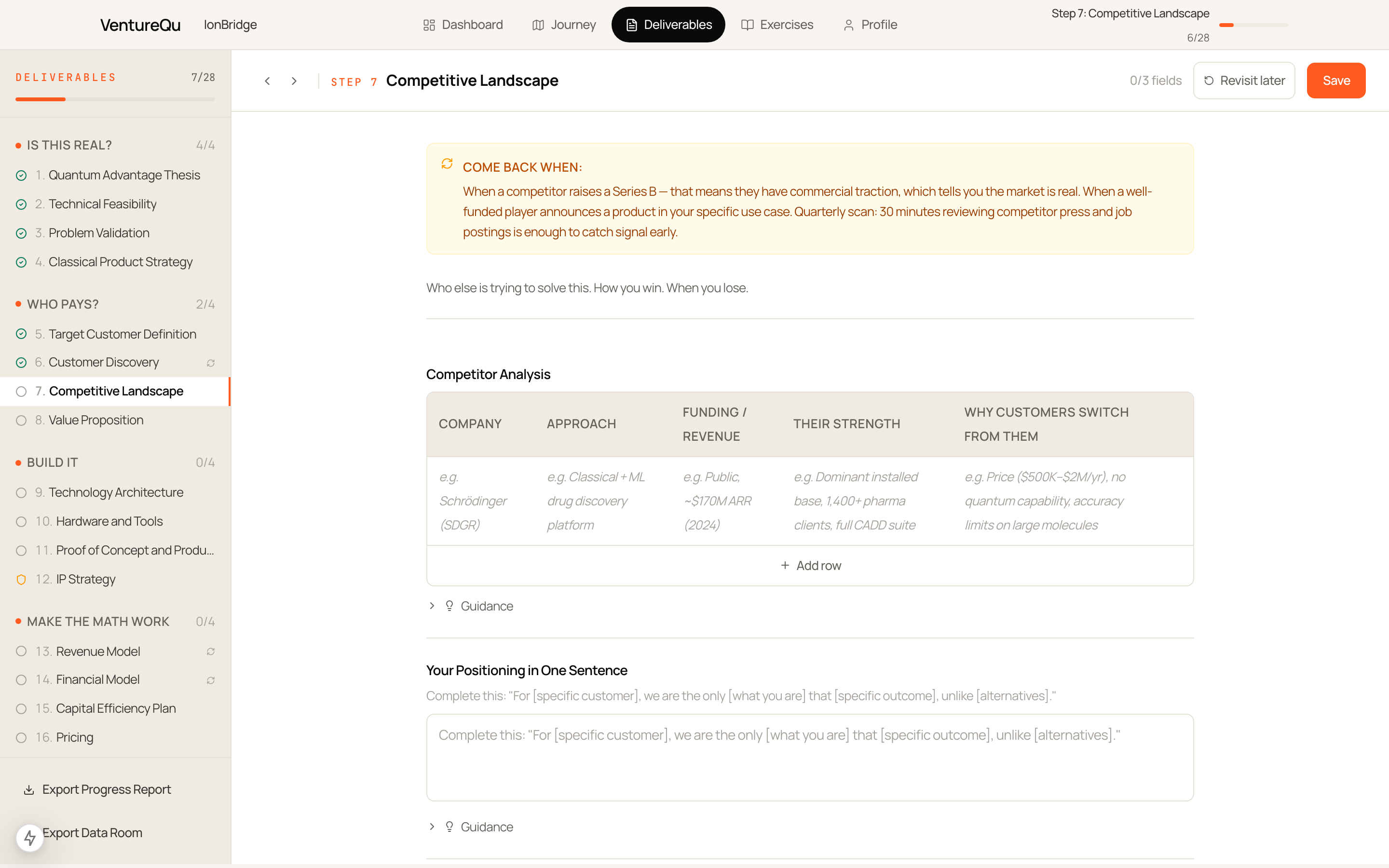

Every piece of work is a filled-in template, not a prompt to an empty document. Competitor tables. Revenue models. IP strategies. Each field comes with a warning about how it usually goes wrong — and what it looks like when it is right.

Short. Specific. Written in the voice of someone who has sat in the room where the question got asked. Pitfalls named by the actual company that made them. Consulting prose has been quietly deleted.

Reads the founder's own work before it answers. Won't let them skip ahead to the exciting part. Refuses to invent a number that isn't grounded. A surprising amount of value comes from the advisor declining to help.

A founder who has already been interrogated by a simulated partner at a Series A firm is a different founder in the real meeting. Practice is cheap. The meeting is not.

Four points in the journey where someone has to decide, on record, to keep going. This is the quiet superpower for anyone allocating capital: an agreed place in advance to stop, so that stopping does not require a fight.

Nine companies in the sector raised more than $100 million each. Combined revenue across the nine is below ten million. That is not a physics problem. It is a reading-the-instruments problem, and it is sitting in somebody's book right now.

VentureQu runs inside a fund, a studio, a cohort. Every company you back produces the same shape of evidence. What is validated, what is assumed, what a partner will ask at the next round. You can read across the book in one place. Founders walk into their partner meetings already knowing what they will be asked. You keep the seat and the relationship. We keep the method current.

Product strategy

Weak quantum-advantage theses drop out before the money is spent.

IP & revenue model

Unsustainable burn is cut. A real revenue model is on the table.

First paying customer

No paying customer means no Series A. The round waits, or doesn't happen.

Kill switch

Ventures that can't earn the next round are closed honestly, not bled.

Past Gate 1, weak quantum-advantage theses drop out. Past Gate 2, unsustainable burn is cut. Past Gate 3, no paying customer means no Series A. Past Gate 4, the venture is honestly closed — not quietly left to bleed.

of named quantum pilots never leave the pilot. They do not fail loudly. They quietly do not convert, and the contract quietly does not renew.

quantum companies each raised more than a hundred million dollars. Combined revenue across the nine is less than ten. Capital efficiency under 0.01 is not a price of doing business. It is a fire.

companies studied in detail. Every template field in the product is grounded in a pattern observed across this set, with the specific company named. Nothing invented.

raised by those companies between them. The money was not the constraint. The method for turning the money into a company was.

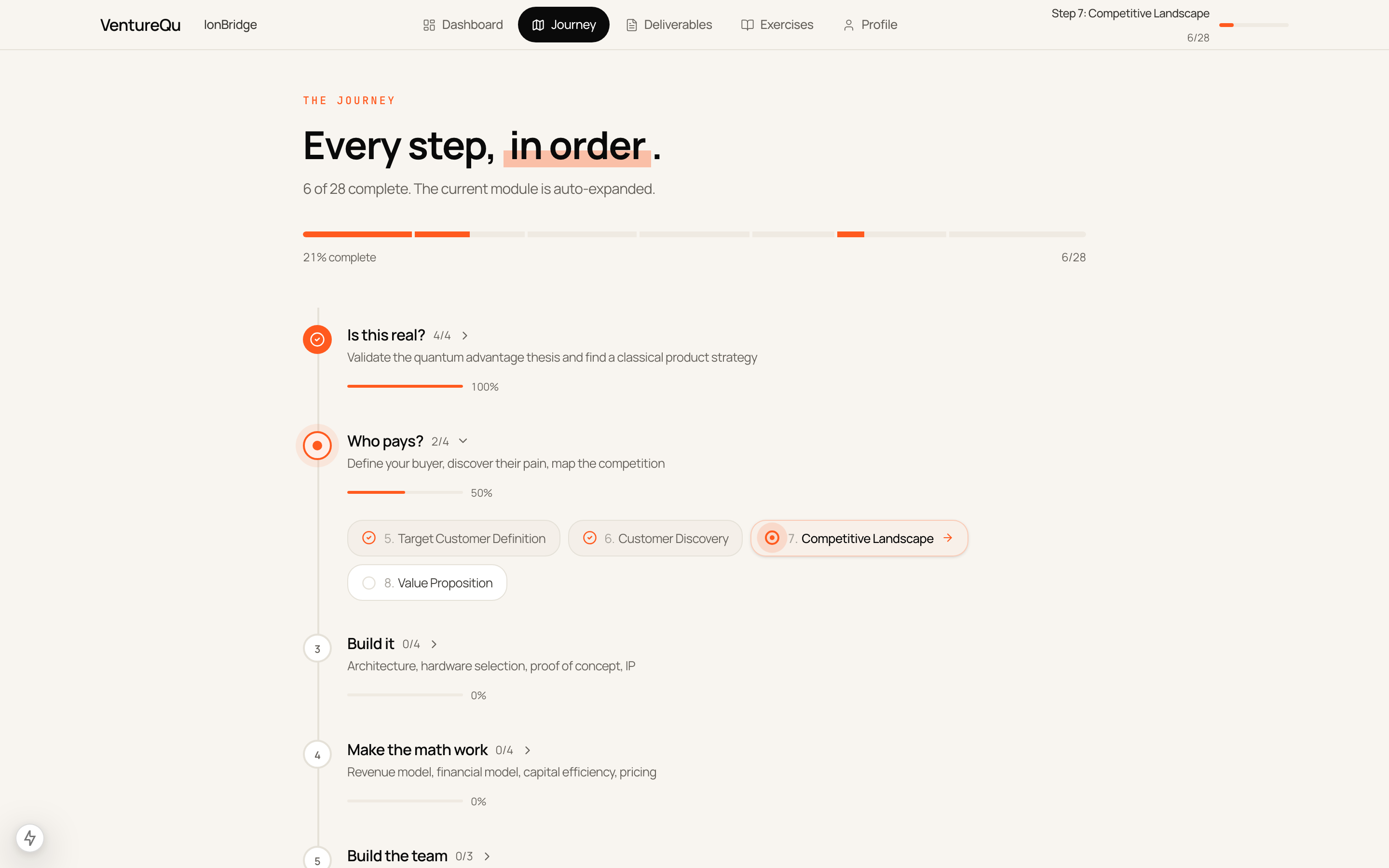

The competitive landscape question is where a lot of quantum ventures start quietly lying to themselves. VentureQu forces the answer to be specific. Real algorithm. Real company. Real outcome. Here is what the founder sees when they open that piece of work.

That is commercial traction by another name, and it tells you the market is real. Or when a well-funded player announces a product in your specific use case. Thirty minutes a quarter on competitor press and job postings catches the signal early enough to matter.

Not "quantum ML" and not "quantum optimization". Name the actual algorithm — QAOA, VQE, Grover's, HHL, QSVM, amplitude estimation — and the software stack. If the answer does not fit on a page, the thinking is not done yet.

Schrödinger runs a drug-discovery platform with classical, ML, and selective quantum inside it. About $170M in ARR as of 2024. QC Ware positioned as "quantum software integration layer," raised $60M, and then pivoted to services. Zapata went public by SPAC and was bankrupt by 2024. Same market, three different stories about what a quantum company is.

Why would a pharma customer switch from their current CADD suite? What happens if an incumbent's QAOA benchmark improves ten-fold in twelve months? A weak answer to this set of questions does not mean more homework. It means the pass gets declined, on record, so the capital moves on.

Every field works this way. Warning. Good-looks standard. A named company. The method is what lives inside these, not the step numbers.

Not opinion.

No invented examples. Every template field is backed by a specific pattern observed across this set — with the named company, the named outcome, and the question a partner will ask in the next round. Method current as of 2026.

VentureQu is a quantum venture-building program delivered as a product. A 28-step workflow in seven modules with four decision gates. Each step has filled-in deliverable templates with warnings, good-looks standards, and a named quantum-company example. Built for the organizations that back quantum founders, and handed to every company on the cap table.

Primary customers are the organizations writing the first quantum check: investment funds, venture studios, corporate investment arms, universities, and research centres. Secondary customers are quantum founders, researchers, and academics, who receive it free by partner invitation.

It is a running workflow, not a deck or a course. Founders open the product and see what to work on today, what good looks like, and which questions will be asked in the next partner meeting. Every field is grounded in real quantum-company data. There is no invented example, no hallucinated benchmark, and no consulting prose.

Gate 1 at Step 4 is product strategy. Gate 2 at Step 12 is IP and revenue model. Gate 3 at Step 23 is the first paying customer. Gate 4 at Step 28 is an explicit kill switch. Gates are decisions made on record. They exist so that saying no does not require a political fight later.

Free for quantum founders, researchers, and academics, by partner invitation. Organizations that deploy VentureQu as part of their portfolio or cohort pay for the platform, co-branded instances, and ongoing method updates.

VentureQu is built on data from 81 quantum companies with $11.8B in tracked funding. 52% of named quantum pilots never convert. Nine companies each raised over $100M with combined revenue under $10M. Every template field references a real company and a real outcome.

Yes. VentureQu is a DeployQuantum solution. DeployQuantum is the quantum readiness platform; VentureQu is the venture-building stack inside that ecosystem.

VentureQu is free for quantum founders, researchers, and academics. You don't pay for it. A partner wrote you in, or you're here early. We onboard cohorts as partners come online.